Another significant change in the Canada Pension Plan (CPP) program takes effect this year. Starting in 2019, the Canadian government initiated a series of improvements and adjustments to the CPP program. The goal of these changes is to provide Canadians with increased benefits and financial security through a modest increase in CPP contributions. It affects and individuals who are employed and make CPP contributions in 2019 or later. What is CPP? First, let’s walk you through the basic information about CPP. If you’re a new employee or not a Canadian resident, you may be wondering what the CPP is. The Canada Pension Plan (CPP) is a compulsory public pension plan in Canada designed to offer essential financial assistance to retired, disabled, or deceased workers and their families. Funding for the CPP comes from contributions made by employees, employers, and self-employed individuals. All employees who work in Canada (outside of Quebec) between the ages of 18 and 70 must make mandatory contributions to the CPP. Employees and employers contribute equally to earnings falling between the Basic Exemption amount and the Year’s Maximum Pensionable Earnings (YMPE). Individuals who have contributed to the CPP for at least one year become eligible to receive retirement benefits upon reaching the age of 65. You can also start receiving as early as age 60 or as late as age 70.

What is new for CPP in 2024?

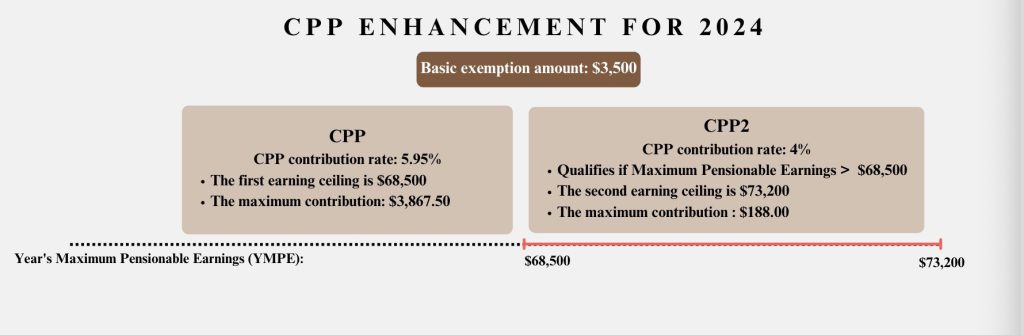

The basic exemption amount for 2024 will remain unchanged at $3,500.

The maximum pensionable earnings to $68,500, an increase from the $66,600 limit in 2023.

CPP contribution rates for both employees and employers remain unchanged at 5.95% in 2024.

The maximum contribution for each is set at $3,867.50—an increase from $3,754.45 in 2023.

CPP2:

Beginning in 2024, a second, higher earnings limit of $73,200, will be introduced to extend Canada Pension Plan (CPP) protection to more of your earnings. This enhanced CPP is called the “year’s additional maximum pensionable earnings” or CPP2.

In 2024, the CPP2 contribution rates for both employees and employers will be 4.00%. The maximum contribution of CPP2 will be $188.00 for each.

Employees will experience the effects of the CPP enhancements on their payroll and in their retirement benefits.

The increased CPP contributions will lead to higher retirement, survivor, and disability pensions for all individuals who contribute. This means that as an employer, you will also be responsible for submitting the increased CPP contributions with the Canada Revenue Agency (CRA) to comply with the CRA.

Please note that When filing T4 slips for the calendar year 2024 and onward, there is a new box (Box 16A) for the employee’s second CPP contributions (CPP2).